Class 10 Economics

Chapter 1 Government Finance (Public Finance)

For SEE Board Exam Preparation: Complete Theoretical Notes and Full Exercise Solutions

Welcome to the complete study guide on Chapter 1 Government Finance under Macroeconomics. This is Chapter 1 of Unit 3 for Class 10 Economics students in Nepal preparing for their SEE board exams.

Here you will find summarized theoretical notes, clear breakdowns of the budget formulation process in Nepal, and fully solved textbook exercises along with additional and numerical problems.

Explore our complete study list here: Class 10 Economics Notes.

1. Theoretical Notes Summary

(A) Introduction to Government Finance

Government Finance (Public Finance) is an important branch of economics that studies the government’s income, expenditure, loans, grants, and the policies and laws related to revenue and expenditure. It examines the sources from which the government earns its income and the heads under which it spends that income.

Key Definitions:

Adam Smith: “Government Finance is the study of the nature and principles of state income and expenditure.”

Dalton and Findlay Shirras: “Government Finance is the science related to the income and expenditure of public bodies.”

(B) Importance of Government Finance

In every welfare state, government finance is crucial for maintaining economic stability and the welfare of citizens. Its key roles are as follows:

(C) Sources of Government Revenue

The main sources of government income can be classified into three broad categories:

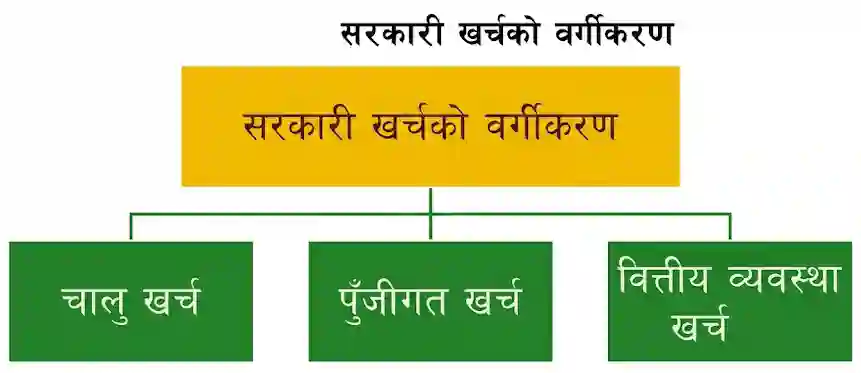

(D) Classification of Government Expenditure

The total expenditure made by the government for public welfare is mainly classified into three categories:

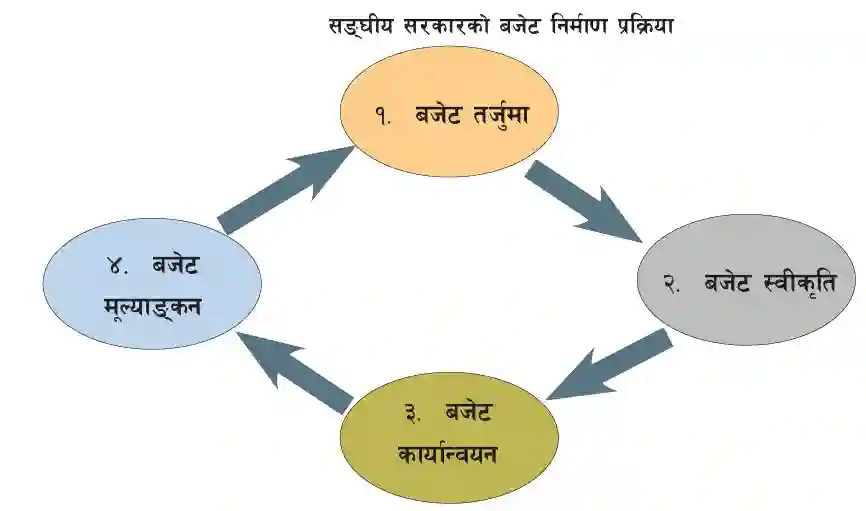

(E) Government Budget and Nepal’s Budget Formulation Process

A budget is a financial plan that outlines the government’s estimated income and proposed expenditure for the upcoming fiscal year. Nepal began presenting budgets from B.S. 2008 (1951 AD). The main types of budget are:

Four Main Stages of Federal Budget Formulation:

2. Exercise — With Solutions

Very Short Answer Questions [1 Mark]

3. Exercise: Short Answer Questions [5 Marks]

According to Adam Smith, “Government Finance is the study of the nature and principles of state income and expenditure.” In the context of Nepal, all three tiers of government — federal, provincial, and local — each maintain their own Consolidated Fund and manage and mobilize public finance through their annual budgets.

1. Direct Tax: This is a tax that must be paid by the very person or institution on whom it is levied; its burden cannot be shifted to anyone else. Examples include: personal and corporate income tax, and property tax.

2. Indirect Tax: This is a tax levied on the consumption of goods and services. Its burden shifts from the producer through to the final consumer. The following taxes fall under this category:

Based on the balance between income and expenditure, a budget is divided into three types:

4. Long Answer Questions [8 Marks]

In the context of Nepal, government expenditure is mainly classified into three categories:

5. Additional Questions & Solved Numericals

(Extra Q&A and Numerical Problems)

Section ‘A’: Very Short Answer Questions

Section ‘B’: Short and Long Answer Questions

i. Tax Revenue: Tax is the amount that citizens must pay to the government without expecting any direct benefit in return. It is the largest source of income for the Government of Nepal. Tax revenue is further divided into two parts:

ii. Non-Tax Revenue: Revenue received by the government from sources other than taxes, through administrative or commercial activities, is called Non-Tax Revenue. Its sources include:

Government expenditure plays an enormously important role in the overall economic development of underdeveloped and developing countries, which can be clarified under the following points:

| S.N. | Estimated Expenditure Heads | Allocated Amount (Rs.) |

|---|---|---|

| 1. | Bus / Transportation Expenses | 30,000 |

| 2. | Hotel / Accommodation Expenses | 20,000 |

| 3. | Main Meals (Breakfast / Dinner) | 15,000 |

| 4. | Snacks and Dry Food Expenses | 5,500 |

| 5. | Entry Fees / Taxes at Tourist Sites | 4,000 |

| 6. | Tour Guide and Driver Allowance | 5,000 |

| 7. | Accompanying Teachers’ Allowance | 4,500 |

| 8. | First Aid and Medicine Kit | 1,500 |

| 9. | Entertainment and Cultural Programs | 2,500 |

| 10. | Miscellaneous / Contingency Expenses | 2,000 |

| Total Estimated Expenditure | 90,000 | |

(Note: Since the total income collected from students is Rs. 90,000 and the total expenditure above is also Rs. 90,000, this is a Balanced Budget.)

Merits of Progressive Tax:

Demerits of Progressive Tax:

Advantages of Indirect Tax:

Disadvantages of Indirect Tax:

Advantages of Direct Tax:

Disadvantages of Direct Tax:

Characteristics of Direct Tax:

Characteristics of Indirect Tax:

1. Proportional Tax: If the tax rate (percentage) remains the same for everyone regardless of how low or high their income is, it is called a Proportional Tax.

Example:

| Income (Rs.) | Tax Rate (%) | Tax Amount Payable (Rs.) |

|---|---|---|

| 10,000 | 10% | 1,000 |

| 40,000 | 10% | 4,000 |

(Here, even though income is different, the tax rate is always 10%.)

2. Progressive Tax: A system in which the tax rate (percentage) increases progressively as a person’s income or wealth increases is called a Progressive Tax. It places a greater burden on the wealthy and a lesser burden on the poor.Example:

| Income (Rs.) | Tax Rate (%) | Tax Amount Payable (Rs.) |

|---|---|---|

| 10,000 | 5% | 500 |

| 40,000 | 35% | 14,000 |

(Here, as income increases, the tax rate has risen from 5% to 35%.)

3. Regressive Tax: A system in which the tax rate (percentage) decreases as a person’s income increases is called a Regressive Tax. This makes the poor even poorer.Example:

| Income (Rs.) | Tax Rate (%) | Tax Amount Payable (Rs.) |

|---|---|---|

| 10,000 | 10% | 1,000 |

| 40,000 | 7% | 2,800 |

(Here, as income increases, the tax rate has fallen from 10% to 7%.)

Importance of Budget: Especially for developing nations like Nepal, the budget is not a mere set of accounts but rather the primary driver of the country’s all-round economic development. Its importances are as follows:

📚 Also Read: Class 10 SEE Notes

Compulsory Subjects

Optional Subjects