Class 10 Economics

Chapter 2 Cost and Cost Curves

For SEE board exam preparation: Complete theoretical notes, graphs, fully solved textbook exercises and numerical problems

Welcome to the complete study guide on Cost and Cost Curves under Microeconomics. This is Chapter 2 of Unit 2 for Class 10 Economics students in Nepal preparing for their SEE board exams.

Here you will find structured notes on all short-run cost concepts — including Total Fixed Cost (TFC), Total Variable Cost (TVC), Total Cost (TC), Average Fixed Cost (AFC), Average Variable Cost (AVC), Average Total Cost (ATC), and Marginal Cost (MC) — along with clear graph illustrations and fully solved textbook exercises with step-by-step numerical solutions.

Explore our complete study list here: Class 10 Economics Notes.

1. Theoretical Concepts: Chapter 2 Cost and Cost Curves

Introduction to Cost

The expenditure incurred on the factors of production during the production process is called cost. Such expenditure can generally be measured in monetary terms. Cost is divided into short-run cost and long-run cost based on the factors of production used. Short-run cost is further studied by dividing it into fixed cost and variable cost. In this chapter, we will study only short-run costs.

(A) Meaning of Cost

To produce the various goods and services we use in our daily lives — such as food, clothing, mobile phones, televisions, notebooks, pens, and so on — the factors of production are required. The major factors of production include land, capital, labour, and organisation, while supporting inputs such as raw materials, energy, communications, and transportation are also needed.

In the production process, land receives rent, capital receives interest, labour receives wages, and organisation receives profit as the reward for using those factors. Similarly, for using inputs such as raw materials, energy, communications, and transportation, their respective prices, fees, and charges must be paid. The total expenditure made on all these factors of production during the production process is called cost.

(B) Short-Run Cost and Cost Curves

In economics, the short run refers to a time period in which not all factors of production can be changed — some factors remain fixed while others are variable. The total expenditure incurred on both fixed and variable factors of production in this period is called short-run cost. For example, a farmer producing rice keeps the area of agricultural land constant (a fixed factor) while adjusting the amount of labour, seeds, and fertilisers (variable factors) as needed. The cost the farmer incurs while producing rice is called short-run cost, because land is used as a fixed factor and the others as variable factors. The expenditure on both types of factors is called short-run cost.

Under short-run cost, Total, Average, and Marginal costs are discussed below:

(i) Total Cost and Total Cost Curves

The total expenditure incurred in producing a given quantity of goods and services is called Total Cost. In the short run, this is the sum of all expenditure on every type of factor of production. Total Cost is studied by dividing it into the following two parts:

a. Total Fixed Cost (TFC): The expenditure incurred on fixed factors of production — such as land, capital (machinery and equipment), permanent labour, and management — is called fixed cost. Fixed cost remains unchanged throughout the production period. This cost does not change whether production increases or decreases. Even when output is zero, this cost must still be borne. For example, if a shoe-making firm rents a building for Rs. 1,00,000 per year, it must pay that rent whether it produces shoes or not. In this case, the building rent is a fixed cost for the firm.

b. Total Variable Cost (TVC): The expenditure incurred on variable factors of production — such as temporary labour, raw materials, water, electricity, transportation, and packaging — is called variable cost. This cost increases when the quantity of production increases and decreases when it falls. In other words, variable cost changes as the level of production changes. For example, if a shoe factory produces 50,000 pairs of shoes, the cost of raw materials, transportation, and packaging increases accordingly; if it produces only 5,000 pairs, variable cost also falls. When output is zero, this cost is nil. The TVC curve starts from the origin and rises to the upper right. However, since it does not increase at a uniform rate — first rising at a decreasing rate and then at an increasing rate — it takes the shape of an inverted English letter “S”.

c. Total Cost (TC): The sum of Total Fixed Cost and Total Variable Cost is the short-run Total Cost. It is expressed as:

Total Cost (TC) = Total Fixed Cost (TFC) + Total Variable Cost (TVC)

That is, $$TC = TFC + TVC$$

(ii) Average Cost and Average Cost Curves

The cost incurred in producing one unit of a good is called Average Cost. In the short run, average cost is studied by dividing it into the following three parts:

a. Average Fixed Cost (AFC): The quotient obtained by dividing Total Fixed Cost (TFC) by the quantity of output (Q) is called Average Fixed Cost. In other words, it is the fixed cost per unit of output. The formula is:

$$AFC = \frac{TFC}{Q}$$

b. Average Variable Cost (AVC): The quotient obtained by dividing Total Variable Cost (TVC) by the quantity of output (Q) is called Average Variable Cost. It is the variable cost per unit of output. It is calculated as:

$$AVC = \frac{TVC}{Q}$$

c. Average Total Cost (ATC or AC): The quotient obtained by dividing Total Cost (TC) by the quantity of output (Q) is called Average Total Cost. It is also the sum of Average Fixed Cost (AFC) and Average Variable Cost (AVC). Average Total Cost is also simply called Average Cost. It is calculated using the following formulas:

$$ATC = \frac{TC}{Q} \quad \text{or} \quad ATC = \frac{TFC}{Q} + \frac{TVC}{Q} \quad \text{or} \quad ATC = AFC + AVC$$

(iii) Marginal Cost and Marginal Cost Curve

The quotient obtained by dividing the change in Total Cost by the change in quantity of output is called Marginal Cost. In other words, the additional change in Total Cost that occurs when one extra unit of a good or service is produced is called Marginal Cost. It is calculated as follows:

$$MC = \frac{\Delta TC}{\Delta Q} \quad \text{or} \quad MC = \frac{TC_n – TC_{n-1}}{Q_n – Q_{n-1}}$$

where,

$TC_n$ = Total Cost of the succeeding unit

$TC_{n-1}$ = Total Cost of the preceding unit

$Q_n$ = Succeeding quantity

$Q_{n-1}$ = Preceding quantity

2. Exercise (With Solutions)

Very Short Answer Questions [1 Mark]

We know: $TC = TFC + TVC$

Therefore: $TFC = TC – TVC = 1{,}000 – 200 = \text{Rs. } 800$

Marginal Cost ($MC$) = $TC_{11} – TC_{10} = 225 – 200 = \text{Rs. } 25$

Average Cost ($ATC$) = $\dfrac{TC}{Q} = \dfrac{50{,}000}{20} = \text{Rs. } 2{,}500$

3. Short Answer Questions [5 Marks]

Example: A farmer producing rice keeps the area of agricultural land constant (which is a fixed cost) and adjusts the number of labourers, seeds, and fertilisers as needed (which are variable costs). The total expenditure on both types of factors is the short-run cost.

- Total Fixed Cost (TFC): This is the expenditure incurred on fixed factors of production (such as land, machinery, and building rent). It remains unchanged throughout the production period. Even when output is zero, this cost must still be paid.

- Total Variable Cost (TVC): This is the expenditure incurred on variable factors of production (such as temporary labour, raw materials, and electricity). It increases as the quantity of production increases and decreases as production falls. When output is zero, this cost is also zero.

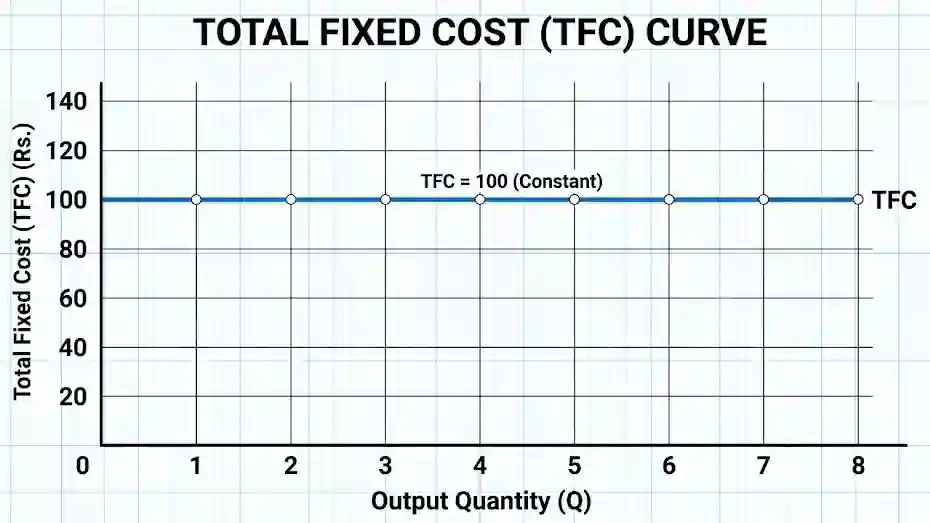

| Quantity of Output (Q) | Total Fixed Cost (TFC) in Rs. |

|---|---|

| 1 | 100 |

| 2 | 100 |

| 3 | 100 |

| 4 | 100 |

| 5 | 100 |

| 6 | 100 |

Drawing the curve: With the quantity of output (Q) on the X-axis and TFC on the Y-axis, the TFC curve is a horizontal straight line parallel to the X-axis, starting from Rs. 100 on the Y-axis, because no matter how much output increases, the cost remains 100.

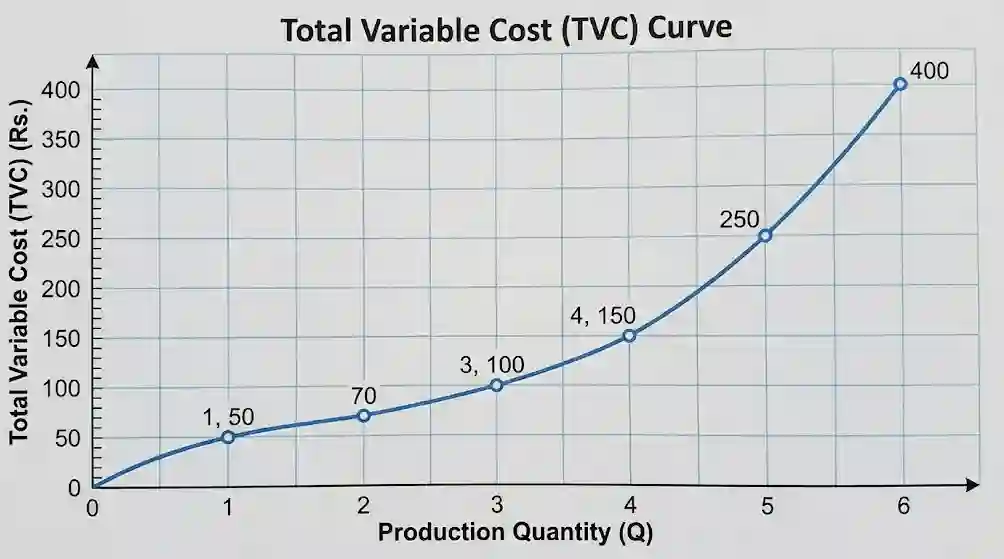

Example: In a shoe factory, the cost of leather (raw material) and transportation for producing 50,000 pairs of shoes is far higher than for producing only 5,000 pairs. If the factory shuts down completely and output falls to zero, the raw material cost (TVC) also becomes zero.

| Quantity of Output (Q) | Total Variable Cost (TVC) in Rs. |

|---|---|

| 0 | 0 |

| 1 | 50 |

| 2 | 70 |

| 3 | 100 |

| 4 | 150 |

| 5 | 250 |

| 6 | 400 |

Drawing the curve: With the quantity of output (0 to 6) on the X-axis and TVC (0 to 400) on the Y-axis, the TVC curve starts from the origin (0, 0). It first rises slowly at a decreasing rate, then increases sharply at an increasing rate — giving it the shape of an inverted “S”.

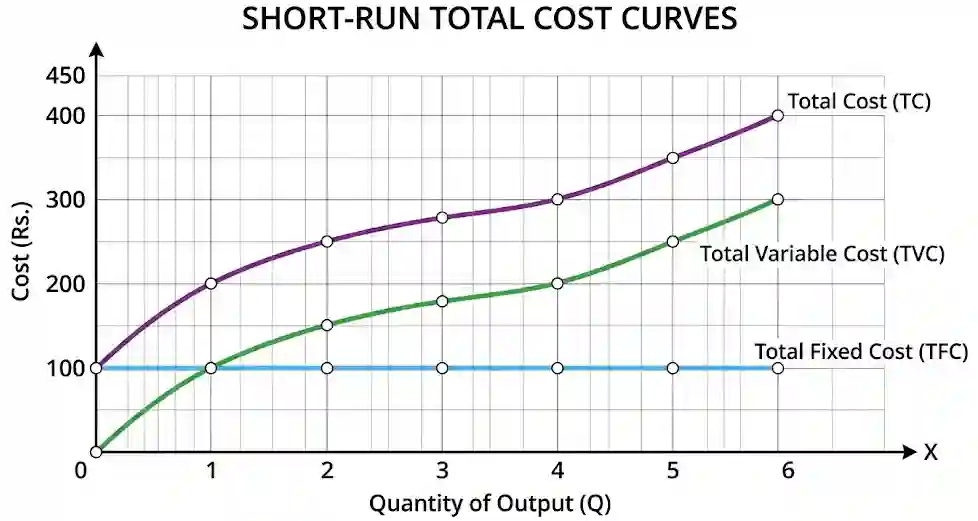

Shape: The TC curve is similar in shape to the TVC curve — it takes the form of an inverted “S”. However, since TFC must still be paid even when output is zero, the TC curve does not start from the origin (0) but from the point on the Y-axis where TFC begins.

Nature in the diagram: With the quantity of output on the X-axis and average cost on the Y-axis, this curve first falls, reaches a minimum at a certain point, and then rises again. Therefore, the Average Total Cost (ATC) curve takes the shape of the English letter “U”.

Reason for the “U” shape: Initially, as production increases, the law of increasing returns applies due to specialisation and division of labour — factors are used most efficiently, causing MC to fall. However, beyond a certain point, adding more variable factors to fixed factors leads to diminishing returns — inefficiency grows and MC begins to rise. Because it first falls and then rises, the Marginal Cost curve takes the “U” shape.

4. Long Answer Questions [8 Marks]

| Quantity of Output (Q) | Total Fixed Cost (TFC) Rs. | Total Variable Cost (TVC) Rs. | Total Cost (TC) Rs. |

|---|---|---|---|

| 0 | 100 | 0 | 100 |

| 1 | 100 | 100 | 200 |

| 2 | 100 | 150 | 250 |

| 3 | 100 | 180 | 280 |

| 4 | 100 | 200 | 300 |

| 5 | 100 | 250 | 350 |

| 6 | 100 | 300 | 400 |

Nature of the Cost Curves:

- TFC Curve: Since it remains constant at Rs. 100, it is a horizontal straight line parallel to the X-axis.

- TVC Curve: Starts from the origin (0) and rises in an inverted “S” shape — first increasing slowly and then more steeply.

- TC Curve: Even when output is zero, TC starts at Rs. 100 (equal to TFC). Its shape is the same as TVC — an inverted “S” — but it always runs parallel to and above the TVC curve by a vertical distance equal to TFC (Rs. 100).

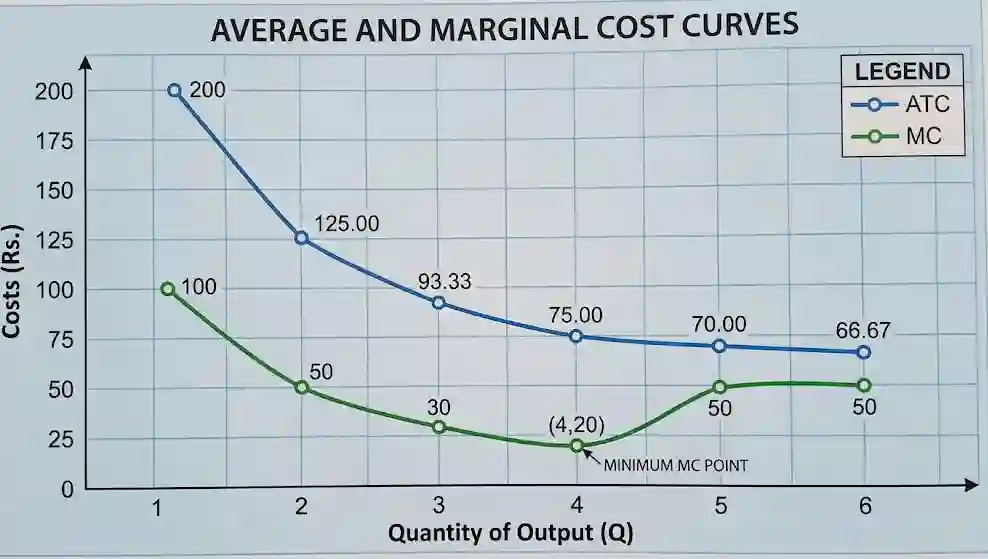

| Quantity (Q) | TVC | Total Cost (TC)* | Average Total Cost (ATC) | Marginal Cost (MC) |

|---|---|---|---|---|

| 0 | 0 | 100 | — | — |

| 1 | 100 | 200 | 200.00 | 100 |

| 2 | 150 | 250 | 125.00 | 50 |

| 3 | 180 | 280 | 93.33 | 30 |

| 4 | 200 | 300 | 75.00 | 20 |

| 5 | 250 | 350 | 70.00 | 50 |

| 6 | 300 | 400 | 66.67 | 50 |

Presentation in the diagram and nature of the curves:

- Average Total Cost (ATC) Curve: From the table, ATC falls from 200 at the 1st unit to 66.67 at the 6th unit. In the diagram, it slopes downward from upper-left and, after reaching its minimum point, begins to rise — forming a “U” shape.

- Marginal Cost (MC) Curve: MC falls from 100 at the 1st unit to its lowest value of 20 at the 4th unit, then rises to 50 at the 5th and 6th units. In the diagram, MC falls quickly to its minimum point and then rises steeply — making a clear “U” shape. The MC curve cuts the ATC curve at ATC’s lowest (minimum) point, where MC = ATC.

5. Additional Exercises

Conceptual and Numerical Questions

- Both are derived from Total Cost (TC).

- Both curves are “U”-shaped.

- When AC is falling, MC lies below AC (MC falls faster than AC).

- When AC is rising, MC lies above AC (MC rises faster than AC).

- The MC curve always cuts the AC curve at AC’s lowest (minimum) point — this is the point where AC = MC.

Solved Numerical Problems

9. If TC = Rs. 500 and TVC = Rs. 200 for producing a good, find the Total Fixed Cost.

$TC = 500$, $TVC = 200$

$TFC = TC – TVC = 500 – 200$

∴ Total Fixed Cost = Rs. 300

10. Ram spends Rs. 1,200 to produce 4 shirts. When he produces 7 shirts, Total Cost rises to Rs. 1,800. Find the Marginal Cost.

$TC_1 = 1{,}200$, $Q_1 = 4$

$TC_2 = 1{,}800$, $Q_2 = 7$

$\Delta TC = 1{,}800 – 1{,}200 = 600$

$\Delta Q = 7 – 4 = 3$

$$MC = \frac{\Delta TC}{\Delta Q} = \frac{600}{3} = \text{Rs. } 200$$ ∴ Marginal Cost = Rs. 200

11. A firm produces 10 units. TFC = Rs. 100 and TC = Rs. 250. Find TVC and AVC.

$Q = 10$, $TFC = 100$, $TC = 250$

$TVC = TC – TFC = 250 – 100 = \text{Rs. } 150$

$$AVC = \frac{TVC}{Q} = \frac{150}{10} = \text{Rs. } 15$$ ∴ TVC = Rs. 150 and AVC = Rs. 15

12. When output rises from 25 to 65 units, Total Cost increases from Rs. 1,780 to Rs. 1,990. Find the Marginal Cost.

$\Delta Q = 65 – 25 = 40$

$\Delta TC = 1{,}990 – 1{,}780 = 210$

$$MC = \frac{\Delta TC}{\Delta Q} = \frac{210}{40} = \text{Rs. } 5.25$$ ∴ Marginal Cost = Rs. 5.25

13. Complete the table below: (Formula: $TC = TFC + TVC$)

| Q | TFC | TVC | TC (Answer) |

|---|---|---|---|

| 0 | 100 | 0 | 100 |

| 1 | 100 | 60 | 160 |

| 2 | 100 | 80 | 180 |

| 3 | 100 | 90 | 190 |

📚 Also Read: Class 10 SEE Notes

Compulsory Subjects

Optional Subjects