Class 10 Economics

Chapter 3 Market Structure and Product Pricing

For SEE board exam preparation: Complete theoretical notes, graphs, fully solved textbook exercises and numerical problems

Welcome to the complete study guide on Chapter 3 Market Structure and Product Pricing under Microeconomics. This is Chapter 3 of Unit 2 for Class 10 Economics students in Nepal preparing for their SEE board exams.

Here you will find structured notes on the meaning of market, its components, types of market (local, national, international), market types based on competition, short-run equilibrium under Perfect Competition and Monopoly using the MC-MR method, along with clear diagram explanations, fully solved textbook exercises, and additional numerical problems.

Explore our complete study list here: Class 10 Economics Notes.

1. Theoretical Concepts

Introduction

Market structure encompasses aspects such as the number of buyers and sellers for a given good, the level of competition, and the manner in which prices are determined. In this chapter, we study how the prices of goods and services are determined under both Perfect Competition and Monopoly market structures, and the key differences between these two types of markets.

(A) Meaning of Market

The word “market” comes from the English word Market, which is believed to have originated from the Latin word Mercatus, meaning trade or commerce. In the ordinary sense, a market is a place where buyers and sellers meet and buy and sell goods and services.

In economics, however, a market refers not just to a physical place of transaction but to the entire process of buying and selling. Therefore, a market is any place or medium — physical or virtual — through which buyers and sellers come into contact and exchange goods and services at an agreed price.

(B) Components of a Market

For a market to exist, the following components are generally required:

- Place or Means of Communication: A market requires either a physical location where buyers and sellers can meet, or a means of communication — such as telephone, email, the internet, or social media — through which they can establish contact even without being physically present in the same place.

- Buyers and Sellers: Buyers and sellers are the two parties to any exchange. Without either party, no transaction can take place. The exchange of goods and services occurs only through the mutual agreement of both buyers and sellers.

- Goods or Services: The mere meeting of buyers and sellers alone does not constitute a market. For a market to function, goods or services that can be bought and sold must be available.

- Willingness and Ability: Both the buyer and the seller must have the willingness to trade. Similarly, both must have the financial or productive capacity to carry out the exchange.

- Price: Since all goods and services exchanged in a market are economic in nature, they carry a definite price. The buyer must be willing to purchase and the seller must be willing to sell at that agreed price.

(C) Types of Market

Markets are classified and studied on the basis of geographical area, level of competition, factors of production, financial assets, time period, and other criteria. Here we classify markets on the basis of geographical area and competition.

(i) On the Basis of Geographical Area

On the basis of their geographical reach, markets are divided into three types:

a. Local Market: When goods and services produced in a specific local area are bought and sold only within that same locality, the market is called a Local Market. These markets typically deal in perishable goods that spoil quickly.

Examples: Weekly or fortnightly rural and urban bazaars (hat bazaar) where fresh vegetables, leafy greens, fish, meat, milk, and dairy products are sold.

b. National Market: When goods produced in one particular region of a country are distributed and sold across various parts of the entire country, that market is called a National Market. Goods traded in a national market are generally durable in nature and can be stored and transported over longer distances.

Examples: Rice grown in the Terai being supplied throughout Nepal; cement produced in Udayapur, Arghakhanchi, or Hetauda being distributed nationwide; tea, cloth, and sugar being traded across the country.

c. International Market: When goods and services are traded not just within a country’s borders but also across different countries of the world, the market is called an International Market. International trade has two sides: exports (goods sent out of the country) and imports (goods brought into the country).

Examples: Gold, vehicles, mobile phones, cameras, and clothing imported from abroad; and Nepal’s ginger, cardamom, tea, coffee, medicinal herbs, and handicrafts exported to foreign countries.

(ii) On the Basis of Competition

On the basis of the degree of competition, markets are divided into two main categories: Perfect Competition and Imperfect Competition. Imperfect competition is further divided into monopolistic competition, oligopoly, monopoly, and monopsony. In this chapter, we focus only on Perfect Competition and Monopoly.

i. Perfect Competition Market: A market structure with a large number of buyers and sellers all producing and trading identical (homogeneous) goods is called a Perfect Competition Market. In this market, the producers are called firms and a group of firms is called an industry. There is no direct rivalry between individual firms. All firms accept the price determined by the market. Therefore, this market is also called a price-taker market. Perfect competition is a theoretical (ideal) market structure that does not fully exist in the real world.

ii. Monopoly Market: A market structure with a single seller and a large number of buyers is called a Monopoly Market. There is only one firm producing a particular good or service, and that firm determines the price. Therefore, this market is also called a price-maker market. No close substitute for the monopolist’s product is available in the market. In the context of Nepal, organisations such as the Nepal Oil Corporation (NOC) and the Nepal Electricity Authority (NEA) function as examples of monopoly markets.

(D) Short-Run Equilibrium under Perfect Competition and Monopoly

Equilibrium refers to the situation in which a firm determines the equilibrium price and equilibrium quantity for its goods or services. To achieve equilibrium under both Perfect Competition and Monopoly, a firm must satisfy the following two conditions:

- Necessary Condition: For a firm to be in equilibrium, its Marginal Cost must equal its Marginal Revenue:

$$MC = MR$$ - Sufficient Condition: For a firm to be in equilibrium, the Marginal Cost curve must intersect the Marginal Revenue curve from below. At the point of intersection, the slope of the MC curve must be greater than the slope of the MR curve:

$$\text{Slope of MC curve} > \text{Slope of MR curve}$$

Using these two conditions and applying the Marginal Cost–Marginal Revenue (MC = MR) method, the short-run equilibrium under both market types is explained below.

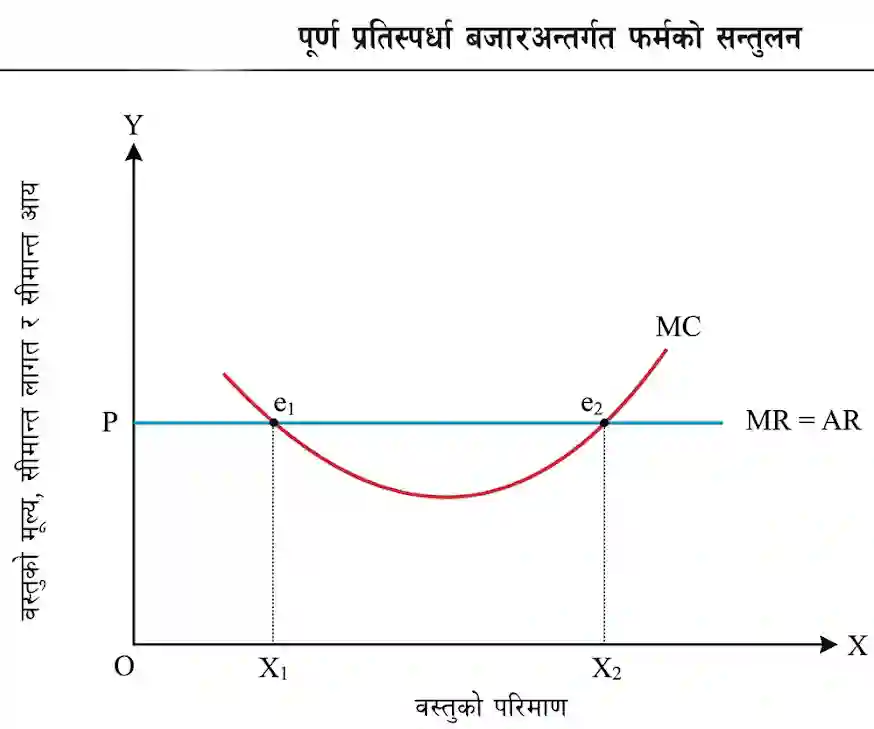

i. Equilibrium under Perfect Competition

A perfectly competitive market is a price-taker market. Since the firm can sell any quantity at the fixed market price, Marginal Revenue (MR) remains constant and equal to the price. Marginal Cost (MC), on the other hand, first falls and then rises as output increases — giving it a “U” shape. The equilibrium of the firm using the MC–MR method is shown in Diagram 3.1 below.

Explanation: In Diagram 3.1, quantity of output is measured on the X-axis and price, Marginal Cost (MC), and Marginal Revenue (MR) are measured on the Y-axis. When the firm produces quantities $OX_1$ and $OX_2$, MC equals MR at points $e_1$ and $e_2$ respectively — satisfying the first (necessary) condition of equilibrium at both points. At point $e_1$, the MC curve intersects MR from above, so the second (sufficient) condition is not fulfilled. However, at point $e_2$, the MC curve intersects the MR curve from below — satisfying both equilibrium conditions. Therefore, $e_2$ is the firm’s equilibrium point. Here, $OP$ is the equilibrium price and $OX_2$ is the equilibrium quantity.

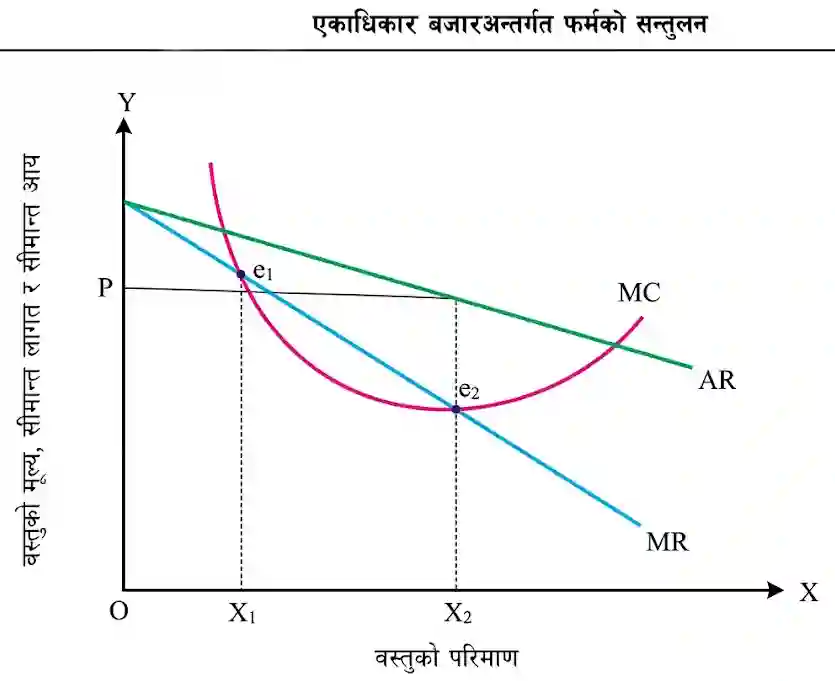

ii. Equilibrium under Monopoly

In a monopoly market, there is only one seller. Since the monopolist must lower the price to sell a larger quantity, the Marginal Revenue (MR) falls continuously as output increases — giving the MR curve a negative (downward) slope. The Marginal Cost (MC) curve, as in perfect competition, first falls and then rises. The MC–MR method for determining firm equilibrium under monopoly is shown in Diagram 3.2 below.

Explanation: In Diagram 3.2, quantity of output is measured on the X-axis and price, MC, and MR are measured on the Y-axis. When the firm produces quantities $OX_1$ and $OX_2$, MC equals MR at points $e_1$ and $e_2$ respectively — satisfying the first condition at both. At point $e_1$, the MC curve crosses MR from above, so the sufficient condition is not met. At point $e_2$, however, the MC curve intersects the MR curve from below — satisfying both equilibrium conditions. Therefore, $e_2$ is the equilibrium point of the monopoly firm. The equilibrium price is $OP$ and the equilibrium quantity is $OX_2$.

(E) Differences Between Perfect Competition and Monopoly Market Structures

Perfect Competition and Monopoly are two diametrically opposite market structures. They differ in terms of the number of sellers, nature of AR and MR, price determination, and entry and exit conditions. The key differences are presented in the table below:

| Differences Between Perfect Competition and Monopoly Markets | |||

|---|---|---|---|

| S.N. | Basis of Difference | Perfect Competition Market | Monopoly Market |

| 1. | Number of Buyers and Sellers | A very large number of both buyers and sellers participate in the market. | There are a large number of buyers but only a single seller. |

| 2. | Nature of the Good | All firms produce homogeneous (identical) goods. | The good produced has no close substitute available in the market. |

| 3. | Entry and Exit | Firms are completely free to enter and exit the industry at any time. | The entry of new firms into the market is completely restricted and prohibited. |

| 4. | Price | The price of the good is uniform (identical) for all buyers and sellers. | The price of the good can differ; the monopolist has control over pricing. |

| 5. | Price Determination | The firm is a price taker — it accepts the price set by the market. | The firm is a price maker — it sets the price itself. |

| 6. | Average and Marginal Revenue | Average Revenue (AR) and Marginal Revenue (MR) are equal and constant. | Marginal Revenue (MR) is less than Average Revenue (AR); both decline continuously. |

2. Exercise (With Solutions)

Very Short Answer Questions [1 Mark]

3. Short Answer Questions [5 Marks]

- Place or Means of Communication: A physical location or communication medium (such as the internet or telephone) where buyers and sellers can meet or connect.

- Buyers and Sellers: The presence of both parties — those who buy and those who sell.

- Goods or Services: Economic goods or services that are available for exchange.

- Willingness and Ability: Both the buyer’s willingness and ability to buy, and the seller’s willingness and ability to sell.

- Price: A definite price agreed upon by both parties for the exchange of goods and services.

- 1. Perfect Competition Market: This is a theoretical (ideal) market structure in which a very large number of buyers and sellers all deal in identical (homogeneous) goods of the same quality and size. No individual firm has any control over the price — all firms are “price takers” and a single uniform price prevails throughout the market.

- 2. Imperfect Competition Market: Any market that lacks the conditions of perfect competition is classified as imperfect competition. It is further divided into four sub-types: monopolistic competition, oligopoly, monopoly, and monopsony. The most significant of these is Monopoly, where there is only one seller but many buyers. The monopolist’s good has no alternative, and the seller itself is the “price maker.”

| S.N. | Basis of Difference | Perfect Competition | Monopoly |

|---|---|---|---|

| 1. | Buyers and Sellers | A very large number of both buyers and sellers exist. | Many buyers exist, but there is only one seller. |

| 2. | Nature of Good | All firms produce homogeneous (identical) goods. | The good produced has no close substitute in the market. |

| 3. | Price Determination | The firm is a price taker — it accepts the market price. | The firm is a price maker — it sets the price itself. |

| 4. | Entry and Exit | Firms have complete freedom to enter and exit the industry. | Entry of new firms is completely prohibited and restricted. |

| 5. | Revenue Curves | Average Revenue (AR) and Marginal Revenue (MR) are equal and constant (horizontal line). | MR is less than AR; both slope downward continuously. |

4. Long Answer Questions [8 Marks]

1. Local Market: A market in which goods and services produced in a particular village, town, or local area are bought and sold exclusively within that same locality is called a Local Market. The goods traded in these markets are usually perishable in nature — they cannot be stored or transported over long distances.

Example: Weekly rural bazaars (hat bazaars) where fresh vegetables, leafy greens, fish, meat, milk, and dairy products produced in the surrounding area are sold locally.

2. National Market: When goods produced in one specific region of a country are distributed and sold across various parts — or throughout the entire country — that market is called a National Market. Goods traded nationally are generally durable in nature and can be safely stored and transported over greater distances.

Examples: Rice grown in the Terai being supplied to all parts of Nepal; cement produced in Hetauda or Udayapur sold nationwide; cloth, furniture, and shoes manufactured in one region being distributed and sold across the whole country.

3. International Market: When goods and services are not confined to one country’s borders but are traded across many different countries of the world, the market is called an International Market. International trade involves two directions: imports (goods brought into the country from abroad) and exports (goods sent out of the country to other nations).

Examples: Gold, vehicles, mobile phones, cameras, and clothing being imported into Nepal from abroad; and Nepal’s tea, coffee, cardamom, ginger, medicinal herbs, carpets, and handicrafts being exported to international markets.

Explanation of the diagram: In the diagram above, the quantity of output is measured on the X-axis and Price (P), Marginal Revenue (MR), and Marginal Cost (MC) are measured on the Y-axis. Since the price is constant, the MR curve is horizontal (parallel to the X-axis). The MC curve is U-shaped. The MC curve intersects the MR curve at two points: $e_1$ and $e_2$. At both points, $MC = MR$ — satisfying the first condition. However, at $e_1$, the MC curve crosses MR from above, so the second condition is not fulfilled. At $e_2$, the MC curve cuts the MR curve from below, satisfying both equilibrium conditions. Therefore, $e_2$ is the firm’s equilibrium point. At this point, the equilibrium price is $OP$ and the equilibrium quantity of output is $OX_2$.

Explanation of the diagram: In the diagram above, output quantity is measured on the X-axis and Price, MR, and MC are measured on the Y-axis. The MR curve slopes downward. The MC curve has a “U” shape. The MC and MR curves are equal at two points: $e_1$ and $e_2$. At $e_1$, the MC curve crosses the MR curve from above, so the sufficient condition for equilibrium is not satisfied (because increasing production beyond this point would still add more to revenue than to cost). At $e_2$, however, the MC curve intersects MR from below, satisfying both conditions. Therefore, $e_2$ is the monopoly firm’s equilibrium point. At this equilibrium, the firm’s price is $OP$ and the equilibrium quantity of output is $OX_2$.

5. Additional Exercises

Conceptual and Numerical Questions

Section A: Very Short Answer Questions

Section B: Short and Long Answer Questions

Four Key Features of Monopoly Market:

- 1. Single Seller and Many Buyers: There is only one firm or producer supplying the good or service in the market, while the number of consumers (buyers) is in the millions.

- 2. No Close Substitute: No alternative product of a similar nature that could replace the monopolist’s good is available anywhere in the market.

- 3. Barriers to Entry: New companies or firms face strict legal, technical, or financial barriers that prevent them from entering the monopolist’s market.

- 4. Firm is the Industry: Since there is only one producer, there is no distinction between the firm and the industry — the single firm represents the entire industry.

Perfect competition is an ideal market condition in which no individual buyer or seller can influence the price of the good. Its main features are:

- 1. Very Large Number of Buyers and Sellers: There are so many buyers and sellers in this market that no single person can affect the overall market price by changing their individual buying or selling behaviour.

- 2. Homogeneous Products: All firms produce goods that are absolutely identical in form, colour, size, quality, and weight. It is impossible to distinguish one firm’s product from another’s.

- 3. Perfect Market Knowledge: Both buyers and sellers have complete information about the market — including the price, quality, and availability of goods in the market at any time.

- 4. Free Entry and Exit: Any new firm may freely enter the industry when existing firms are earning high profits, and may freely exit when it is incurring losses — there are no legal or financial barriers.

- 5. Uniform Price: The single price determined by the overall market forces of demand and supply applies uniformly to all buyers and sellers. Firms are purely price takers — they cannot set or influence the price.

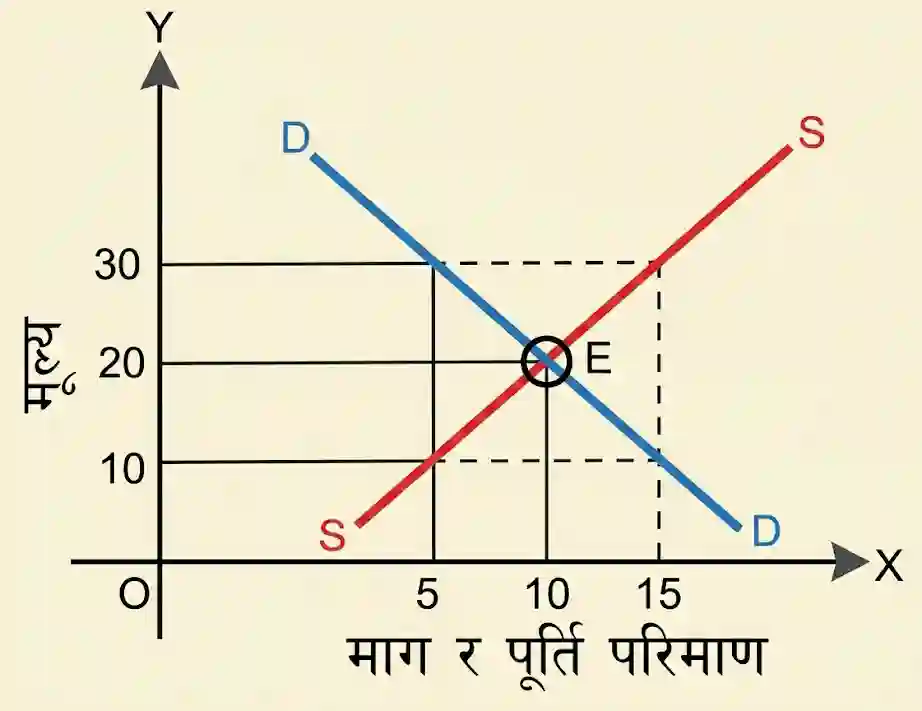

In a perfectly competitive market, no single firm or consumer can dictate the price of a good. The price is determined by the interaction of the total market demand and the total market supply. The price at which the quantity demanded by consumers exactly equals the quantity supplied by producers is called the Equilibrium Price.

Explanation through a table:

| Price (P) | Demand (D) | Supply (S) | Market Condition |

|---|---|---|---|

| 10 | 15 | 5 | Excess Demand (price rises) |

| 20 | 10 | 10 | Equilibrium (Demand = Supply) |

| 30 | 5 | 15 | Excess Supply (price falls) |

In the diagram, the downward-sloping demand curve (DD) and the upward-sloping supply curve (SS) intersect at point E. This intersection point determines the equilibrium price and equilibrium quantity in the market.

- 1. Primary Objective: Regardless of the market structure, the single most important objective of all operating firms is to earn maximum profit (Profit Maximisation) by minimising costs.

- 2. Number of Buyers: In both market structures, the number of consumers (buyers) purchasing the goods is very large.

- 3. Conditions of Equilibrium: In both markets, a firm reaches equilibrium only when the same mathematical condition is satisfied: Marginal Cost equals Marginal Revenue ($MC = MR$), and the MC curve must intersect the MR curve from below.

- 4. Shape of Cost Curves: Because the Law of Variable Proportions operates in production in both markets, the short-run Average Cost (AC) and Marginal Cost (MC) curves in both market structures take the shape of the English letter “U”.

Numerical Problems

5. If a firm’s Total Revenue is Rs. 18,000 and Total Cost is Rs. 13,000, find the Total Profit.

Total Revenue ($TR$) = Rs. 18,000

Total Cost ($TC$) = Rs. 13,000

Profit ($\pi$) = $TR – TC = 18{,}000 – 13{,}000$

∴ Total Profit = Rs. 5,000

6. If Total Cost is Rs. 1,000 and Total Revenue is Rs. 1,200, find the Total Profit.

$TR = 1{,}200$, $TC = 1{,}000$

Profit ($\pi$) = $TR – TC = 1{,}200 – 1{,}000$

∴ Total Profit = Rs. 200

7. If $P = \text{Rs. }30$, $Q = 10$ units, and $AC = \text{Rs. }25$, calculate the firm’s profit.

Price ($P$) = Rs. 30 | Quantity ($Q$) = 10 units | Average Cost ($AC$) = Rs. 25

$TR = P \times Q = 30 \times 10 = \text{Rs. } 300$

$TC = AC \times Q = 25 \times 10 = \text{Rs. } 250$

Profit ($\pi$) = $TR – TC = 300 – 250$

∴ Total Profit = Rs. 50

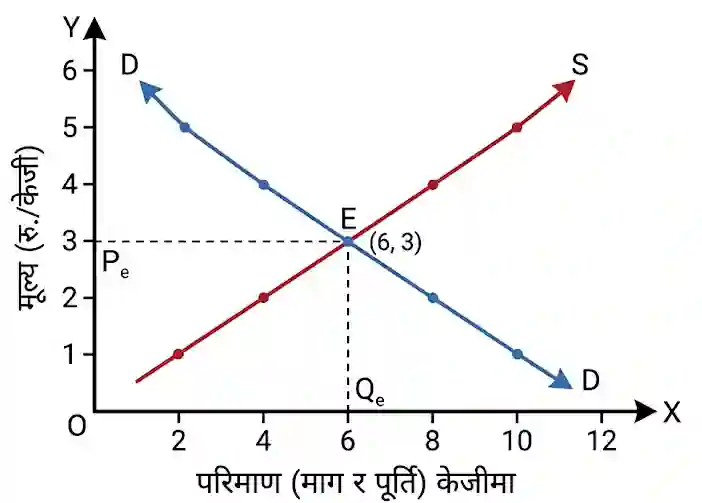

8. Study the table below and answer the questions that follow.

| Market Price (Rs./kg) | Market Demand (kg) | Market Supply (kg) |

|---|---|---|

| 1 | 10 | 2 |

| 2 | 8 | 4 |

| 3 | 6 | 6 |

| 4 | 4 | 8 |

| 5 | 2 | 10 |

a. Draw the market demand and supply curves on the same diagram based on the table above.

b. Based on the diagram, identify the relationship between market price and demand quantity, and between market price and supply quantity.

c. From the diagram, identify the equilibrium price and equilibrium quantity.

📚 Also Read: Class 10 SEE Notes

Compulsory Subjects

Optional Subjects